Difference between Gross Total Income and Total Income & how to compute Gross Total Income and Total Income-

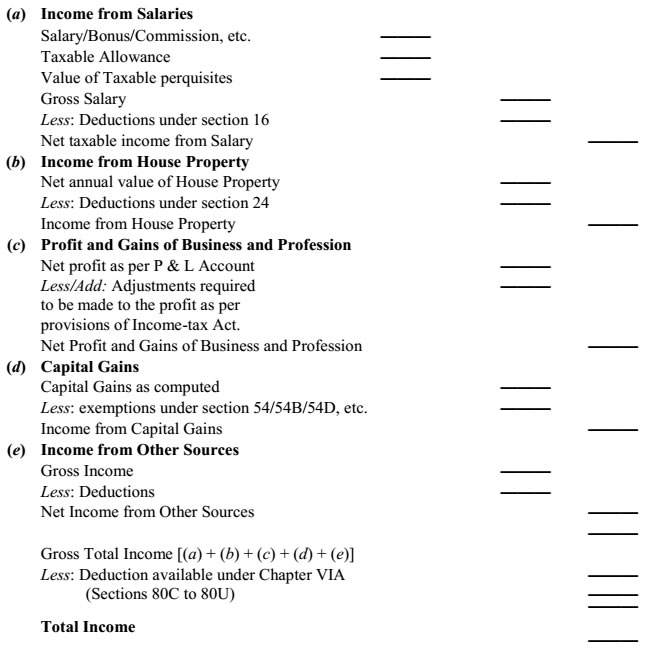

Difference between Gross Total Income and Total Income can be calculated very easily. Every person has source of income from anywhere, all incomes are coming under five heads of income under Income Tax Act i.e.

- Income from Salary

- Income from House Property

- Income from Business or Profession

- Income from Capital Gain

- Income from Other Sources

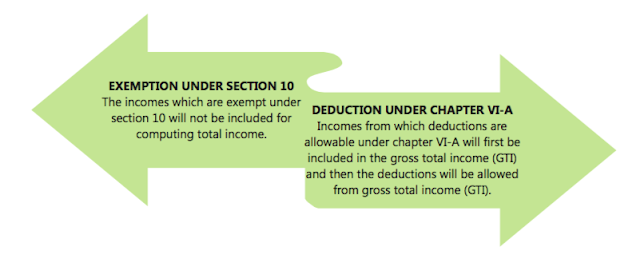

Provision of Clubbing of Income is applicable (included) but Incomes which are exempted under section 10 will be not included in computation of Gross Total Income.

The total income of above five heads are called Gross Total Income and if the deduction falling under category of section 80C to 80U (if any) is deducted from Gross Total Income, the balance taxable income is called Total Income.

Note- Inter source losses, inter head losses, brought forward losses, unabsorbed depreciation, etc., (if any) will have to be adjusted while computing the gross total income.

What is Gross Total Income-

Gross Total Income means Income received from all sources of Income i.e. Income from Salary (if any) +Income from House Property (if any) + Profits and gains of business or profession (if any) + Income from Capital Gain (if any) + Income from other sources (if any).

What is Total Income-

Total Income is the income on which tax liability is determined means Gross Total Income less Deductions (under section 80C to 80U), if any.

How to compute Gross Total Income (GTI) and Total Income-

Example 1-

Mr. X has the following incomes for the financial year 2017-18-

|

Particulars

|

Amount (Rs.)

|

|

Income from Salary (Net of deductions u/s 10 & u/s 16)

|

6,00,000

|

|

Income from House Property (Net)

|

3,00,000

|

|

Income from Business or Profession

|

2,00,000

|

|

Income from Capital Gain

|

50,000

|

|

Income from Other Source (Included Income of Minor Child)

|

2,50,000

|

|

Deduction u/s 80C (Investments)

|

1,50,000

|

|

Deduction u/s 80D (Mediclaim)

|

30,000

|

|

Deduction u/s 80G (Donation)

|

10,000

|

|

Deduction u/s 80TTA (Interest on Savings)

|

10,000

|

|

Deduction u/s 80U (Physical Disability)

|

50,000

|

How to calculate Gross Total Income and Total Income?

Answer-

Computation of Taxable Income of Mr. X, for the year 2017-18

|

Particulars

|

Amount (Rs.)

|

Amount (Rs.)

|

|

|

|

F.Y. 2017-18

|

|

Income from Salary (Net of deductions u/s 10 and u/s 16)

|

|

6,00,000

|

|

Income from House Property (Net)

|

|

3,00,000

|

|

Income from Business or Profession

|

|

2,00,000

|

|

Income from Capital Gain

|

|

50,000

|

|

Income from Other Source (Included Income of Minor Child)

|

|

2,50,000

|

|

Gross Total Income

|

|

14,00,000

|

|

Less: Deductions under Section 80C to 80E

|

|

|

|

Under Section 80C

|

1,50,000

|

|

|

Under Section 80D

|

30,000

|

|

|

Under Section 80G

|

10,000

|

|

|

Under Section 80TTA

|

10,000

|

|

|

Deduction u/s 80U

|

50,000

|

2,50,000

|

|

Total Income (Net Taxable Income)

|

|

11,50,000

|

How to round off total income before computing tax liability?

As per section 288A, total income computed in accordance with the provisions of the Income-tax Law, shall be rounded off to the nearest multiple of ten.

Following points should be kept in mind while rounding off the total income:

- First any part of rupee consisting of any paisa should be ignored.

- After ignoring paisa, if such amount is not in multiples of ten, and last figure in that amount is five or more, the amount shall be increased to the next higher amount which is in multiple of ten and if the last figure is less than five, the amount shall be reduced to the next lower amount which is in multiple of ten and the amount so rounded off shall be deemed to be the total income of the taxpayer.

Example 2-

Total Income of Mr. X comes to Rs. 11, 50,156.88 for the financial year 2017-18. How the total income of Mr. X is rounded off?

Answer-

First the part of rupee consisting of 0.88 paisa should be ignored.

Then after ignoring paisa, the remaining amount of Rs. 11,50,156 shall be rounded off to Rs. 11,50,160 because the last figure is greater than five (i.e. 6 convert to Rs. 10).

Example 3-

Total Income of Mr. X comes to Rs. 11, 50,154.88 for the financial year 2017-18. How the total income of Mr. X is rounded off?

Answer-

First the part of rupee consisting of 0.88 paisa should be ignored.

Then after ignoring paisa, the remaining amount of Rs. 11,50,154 shall be rounded off to Rs. 11,50,150 because the last figure is less than five (i.e. 4 convert to Rs. 0).