Introduction-

Deferred Tax Liability and Deferred Tax Assets is an important part of Financial Statements.

The difference between the books and the taxation income or expense is known as Timing difference which can be classified either as:

- Temporary Difference – the differences between book profits and Profit as per Income tax, which is capable of reversal in subsequent period i.e. Deprecation etc.

- Permanent Difference – When the differences between book profits and Profit as per Income tax, which is not capable of reversal in subsequent period.

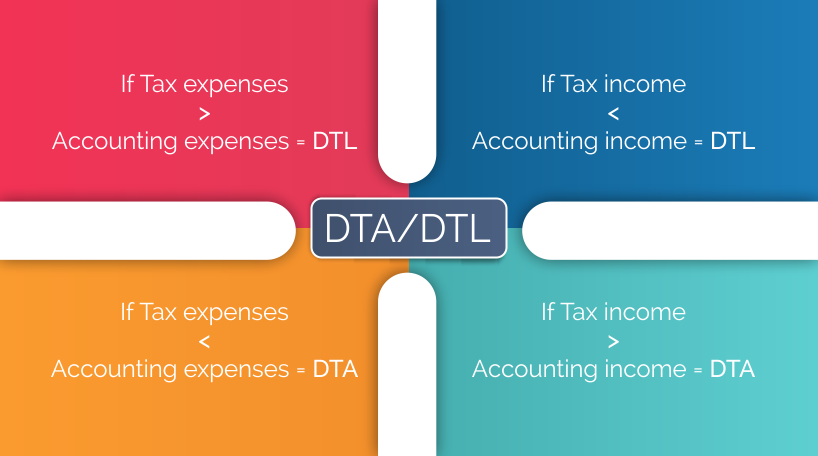

Deferred Tax Liability-

Deferred Tax Liability arises due to timing difference in the value of Assets as per Books of Accounts and as per Income Tax Act. Deferred Tax is purely an accounting Concept. AS 22 - "Accounting for Taxes on Income deals with Deferred Tax.

Example 1- (Temporary Difference)

M/s ABC & Company has profit of Rs. 45.00 lakh during the financial year 2017-18 after charging all expenses but before depreciation of Rs. 5.00 lakh as per books of Accounts but the deprecation under Income Tax Act for the period is Rs. 8.00 lakh. What will be the Deferred Tax liability/Deferred Tax Assets and its treatment in Balance Sheet?

Solution-

|

Particulars

|

As per Books of Accounts

|

As Per Income Tax Act

|

Difference

|

|

Profit before Depreciation

|

45,00,000

|

45,00,000

|

0

|

|

Less: Deprecation

|

5,00,000

|

8,00,000

|

-3,00,000

|

|

Profit Before Tax

|

40,00,000

|

37,00,000

|

3,00,000

|

|

Tax @ 30%

|

12,00,000

|

11,10,000

|

90,000

|

Tax amount as per Books of Accounts is Rs.12,00,000/- but as per Income Tax it is Rs.11,10,000/- the difference of Rs. 90,000 is Deferred Tax Liability which can be reversed in subsequent period.

As Example 1, passed the following entries in your Books of Accounts-

|

S. No.

|

Journal Enteries

|

|

1.

|

Profit & Loss A/c Dr. 11,10,000

To Provision for Income Tax A/c 11,10,000

(Being amount of provision for Income Tax liability)

|

|

2.

|

Profit & Loss A/c Dr. 90,000

To Deferred Tax Liability A/c 90,000

(Being amount of provision of Deferred Tax Liability has made which can be adjusted in future)

|

Example 2- (If entire provision of Deferred Tax Liability has reversed in next year)

M/s ABC & Company has profit of Rs. 50.00 lakh during the financial year 2018-19 after charging all expenses but before depreciation of Rs. 8.00 lakh as per books of Accounts but the deprecation under Income Tax Act for the period is Rs. 5.00 lakh. What will be the Deferred Tax liability/Deferred Tax Assets and its treatment in Balance Sheet?

Solution-

|

Particulars

|

As per Books of Accounts

|

As Per Income Tax Act

|

Difference

|

|

Profit before Depreciation

|

50,00,000

|

50,00,000

|

0

|

|

Less: Deprecation

|

8,00,000

|

5,00,000

|

3,00,000

|

|

Profit Before Tax

|

42,00,000

|

45,00,000

|

-3,00,000

|

|

Tax @ 30%

|

12,60,000

|

13,50,000

|

-90,000

|

Tax amount as per Books of Accounts is Rs.12,60,000/- but as per Income Tax it is Rs.13,50,000/- the difference of Rs. -90,000 is Deferred Tax Assets which will be adjusted from the last year provision of Deferred Tax liability.

As Example 2, Passed the following enteries in your Books of Accounts-

|

S. No.

|

Journal Enteries

|

|

1.

|

Profit & Loss A/c Dr. 13,50,000

To Provision for Income Tax A/c 13,50,000

(Being amount of provision for Income Tax liability)

|

|

2.

|

Deferred Tax Liability A/c Dr. 90,000

To Profit & Loss A/c 90,000

(Being reversal of amount of provision of Deferred Tax Liability created last year)

|

Deferred Tax Asset-

Deferred Tax Assets is similar to Deferred Tax Liability, which also arises due to timing difference in the value of Assets as per Books of Accounts and as per Income Tax Act.

Example 3-

M/s ABC & Company has profit of Rs. 45.00 lakh during the financial year 2017-18 after charging all expenses but before depreciation of Rs. 8.00 lakh as per books of Accounts but the deprecation under Income Tax Act for the period is Rs. 5.00 lakh. What will be the Deferred Tax liability/Deferred Tax Assets and its treatment in Balance Sheet?

Solution-

|

Particulars

|

As per Books of Accounts

|

As Per Income Tax Act

|

Difference

|

|

Profit before Depreciation

|

45,00,000

|

45,00,000

|

0

|

|

Less: Deprecation

|

8,00,000

|

5,00,000

|

3,00,000

|

|

Profit Before Tax

|

37,00,000

|

40,00,000

|

-3,00,000

|

|

Tax @ 30%

|

11,10,000

|

12,00,000

|

-90,000

|

Tax amount as per Books of Accounts is Rs.11,10,000/- but as per Income Tax it is Rs.12,00,000/- the difference of Rs. -90,000 is Deferred Tax Assets which can be adjusted in subsequent period.

As Example 3, Passed the following entries in your Books of Accounts-

|

S.No.

|

Journal Enteries

|

|

1.

|

Profit & Loss A/c Dr. 12,00,000

To Provision for Income Tax A/c 12,00,000

(Being amount of provision for Income Tax liability)

|

|

2.

|

Deferred Tax Assets A/c Dr. 90,000

To Profit & Loss A/c 90,000

(Being amount of balance of Deferred Tax Assets has created which can be adjusted in future from Deferred Tax Liability)

|

Example 4- (If entire balance of Deferred Tax Assets has adjusted in next year)

M/s ABC & Company has profit of Rs. 60.00 lakh during the financial year 2018-19 after charging all expenses but before depreciation of Rs. 5,00 lakh as per books of Accounts but the deprecation under Income Tax Act for the period is Rs. 8.00 lakh. What will be the Deferred Tax liability/Deferred Tax Assets and its treatment in Balance Sheet?

Solution-

|

Particulars

|

As per Books of Accounts

|

As Per Income Tax Act

|

Difference

|

|

Profit before Depreciation

|

60,00,000

|

60,00,000

|

0

|

|

Less: Deprecation

|

5,00,000

|

8,00,000

|

-3,00,000

|

|

Profit Before Tax

|

55,00,000

|

52,00,000

|

3,00,000

|

|

Tax @ 30%

|

16,50,000

|

15,60,000

|

90,000

|

Tax amount as per Books of Accounts is Rs.16,50,000/- but as per Income Tax it is Rs.15,60,000/- the difference of Rs. 90,000 is Deferred Tax Liability which will be adjusted from the last year balance of Deferred Tax liability.

As Example 4, Passed the following entries in your Books of Accounts-

|

S. No.

|

Journal Enteries

|

|

1.

|

Profit & Loss A/c Dr. 15,60,000

To Provision for Income Tax A/c 15,60,000

(Being amount of provision for Income Tax liability)

|

|

2.

|

Profit & Loss A/c Dr. 90,000

To Deferred Tax Assets A/c 90,000

(Being adjusted full amount of last year’s balance of Deferred Tax Assets)

|

Example 5- (If entire provision of Deferred Tax Liability has reversed in subsequent years)

After considered the figures of example 1 (as above), the Provision of Deferred Tax liability has Rs. 90,000 for the financial year 2015-16 standing in our books and the firm has tax difference in subsequent years are as under-

Solution-

|

Particulars

|

2016-17

|

2017-18

|

2018-19

|

2019-20

|

|

Tax as per Books of Account

|

2,70,000

|

3,20,000

|

2,50,000

|

4,20,000

|

|

Tax as per Income Tax

|

3,05,000

|

3,45,000

|

2,70,000

|

4,30,000

|

|

Difference

|

-35,000

|

-25,000

|

-20,000

|

-10,000

|

As Example 5, Passed the following entries in your Books of Accounts-

|

S. No.

|

Journal Enteries 2016-17 2017-18 2018-19 2019-20

|

|

1.

|

Profit & Loss A/c Dr. 3,05,000 3,45,000 2,70,000 4,30,000

To Provision for Income Tax A/c 3,05,000 3,45,000 2,70,000 4,30,000

(Being amount of provision for Income Tax liability)

|

|

2.

|

Deferred Tax Liability A/c Dr. 35,000 25,000 20,000 10,000

To Profit & Loss A/c 35,000 25,000 20,000 10,000

(Being reversal of provision of Deferred Tax Liability)

|